A capital allocator’s culture

Introduction

In my first conversation with Guy Spier about writing a white paper, I mentioned to him that I have a list of individuals I thought of interviewing. “Do you have an opinion on which person I should interview?” I asked, “Whoever is better you,” Guy answered. I was surprised by this unusual answer that I had never heard before.

After publishing the white paper “Doing scuttlebutt on company culture”, I sent the paper to several CEOs of companies known for their unique culture. I didn’t expect to receive an answer, but surprisingly, I did receive one email back. It was Constellation Software’s founder and CEO, Mark Leonard.

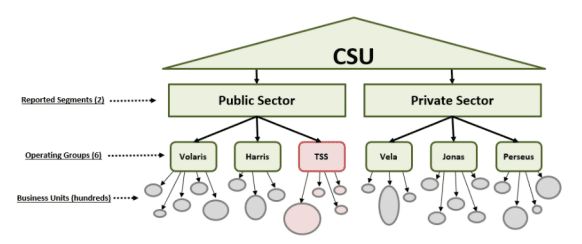

Constellation Software Inc. (CSI), founded in 1995 by former venture capitalist Mark Leonard, is a leading Canadian vertical market software and services provider. The company acquires, manages and builds industry specific software businesses which provide specialized, mission-critical software solutions that address the particular needs of the customers. The company went public in 2006 and is listed on the Toronto Stock Exchange. Constellation has approximately 25,000 employees spread over six operating segments.

Regularly, I heard about Constellation Software and its culture that allows it to achieve exceptional performance in the form of growth, profitability, and, as a result, a stock performance that made the patient shareholder very wealthy – including Mr. Leonard himself who is the fifth major investor in the company. Since May 2006, the company’s stock rose 11,326% (more than 113 fold), dividends excluded, compared to 85% and 244% for the S&P/TSX 60 index and S&P500 index, respectively.

How important is culture to Constellation Software? It turns out to be so important that a culturerelated director – Lawrence Cunningham, was nominated a few years ago. Cunningham is also the author of several best-seller business books and received the permission of Warren Buffett himself to research Berkshire Hathaway’s corporate culture and write about it. Cunningham testifies that the company’s unique culture was a very important part of his decision to join Constellation Software’s directorate.

After receiving Mark Leonard’s email, I received an additional email from Mr. Cunningham emphasizing the importance of the subject to them. If this company’s management gives culture such a high priority,

it might be very interesting to explore its culture further, I thought to myself; there’s must be something

very special about this company.

“While there are terrific moats around our individual business units, the barrier to starting a “conglomerate of vertical market software businesses” is pretty much a cheque book and a telephone. Nevertheless, CSI does have a compelling asset that is difficult to both replicate and maintain: We have 199 separately tracked business units and an open, collegial, and analytical culture.” Mark Leonard, Constellation Software President’s letter 2014

I thought it might be of the reader’s interest to explore what made Constellation Software’s culture so extraordinary over the years. During this process, four central repeated values appeared to me. These values seem fundamental to CSI: Trust, Execution, Long-Term horizon and Conservatism. I would be willing to take it further and suggest those values work very well specifically for holding companies that execute them well enough.

This paper will not focus on the technical parameters and financial analysis of Constellation Software but rather on the company’s core values as they appeared to me mostly: mainly from CSI’s public material, published interviews with senior employees and investors, personal interviews, and blogs, as well as some academic books and articles.

A statement of Mark Leonard in the last annual general meeting of Constellation made me aware of the challenge in trying to analyze this company’s culture. He stated that Constellation Software has no culture as one organization! “I don’t believe we have a culture...the culture of our business that does paratransit in the Nordics is going to be different than the culture of our payroll business in Brazil.” He said. This statement made me much more modest as I approached the task. Alternatively, the reader might choose to see the content below as an attempt to identify shared values among Constellation Software’s many sub-cultures.

1Trust

Trust is a paramount value at Constellation; it appeared to me in several of the company’s elements:

-

- Decentralized structure

“My hunch is that it takes an unusually trusting culture and a long investment horizon to support a

multitude of small businesses and their entrepreneurial leaders. If trust falters the BU’s can be choked by

bureaucracy. If short term results are paramount, the siren song of consolidation synergies is powerful.

We continue to believe that autonomy and responsibility attract and motivate the best managers and

employees.” Mark Leonard, Constellation Software President’s letter 2015

As known to many investors and to each person I was speaking with, Constellation has a decentralized structure. Its mission is spread across the company, authority is delegated, and each business unit acts as an independent entity. Trust is “a must” in such an environment while employees feel the responsibility management gives them. This characteristic may remind the reader of Berkshire Hathaway. Warren Buffett is well known as an old time supporter of a decentralized structure and leads it in his own company. Buffett is known for working with managers he can count on, who have a lot of integrity, abilities and energy, traits that can make him calm and confident that the businesses he owns are in the right hands. As mentioned in the last white paper, “Doing Scuttlebutt on Company Culture”, in a business where participants are honest and of high quality, individuals that care about the business and have work ethics, there is much higher probability that additional such individuals would be raised and promoted throughout the organization while the less competent ones would drop. That way the company’s DNA, its culture, is created, developed and preserved.

If someone is looking for evidence for decentralized culture, he should probably look for the number of employees in the headquarters compared to the total company. In Constellation software, a company with approximately 25,000 employees, only ten people sit in the headquarters at Toronto (a ratio of 1:2,500). Other great examples are Constellation’s neighbor, the Canadian convenience retailer Alimentation Couche-Tard with a ratio of 1:7,000 and of course Berkshire Hathaway with a ratio of 1:14,000

Mark Leonard took trust one step further: unlike Berkshire, the decentralized structure of Constellation includes capital allocation – Leonard also delegates this authority to the operating groups’ managers. Such a structure allows the company to continue and make more attractive acquisitions with each portfolio manager responsible for a concentrated number of positions between 2-12. This allows a portfolio manager to know his portfolio companies and also enables Constellation to preserve the low enterprise value of the acquired companies. In other words, this characteristic about constellation is what makes its business model scalable, and trust is practically reinforcing the company competitive advantage.

-

- Shared knowledge

Like Berkshire that functions as a “greenhouse” for its subsidiaries which can share the vast knowledge accumulated in the organization with each other, in Constellation Software, this sharing theme works as a well oiled machine with specific best practices accumulated during many years and shared between acquired companies – and there are many of them, around 600 companies under one big greenhouse. I found Constellation’s ability to transfer its investment philosophy, its best practices and playbook from the headquarters throughout the operating groups and business units in a unified systematic way, an astonishing achievement.

-

- Role models

Trust starts from the top of the organization. In Constellation, employees emphasize their trust in the management and especially in Mark Leonard. One of the issues discussed in the last paper is that in some cases the presence of one unique leader can create a meaningful difference in the company. Girish Bakhoo has mentioned such examples in Microsoft, Fiat-Chrysler and MasterCard. From reading and interviewing individuals, it seems that Mark Leonard, beyond him being a great manager, phenomenal capital allocator and the face of the company in front of investors, is first and foremost a great role model for the whole organization. Individuals mentioned that his humility and hard work affect employees. It has been told that many employees were chosen in light of Leonard’s traits. They are modest, they are under the radar and avoid publicity, they try to build something valuable, and they are honest. Despite the role model Leonard plays and the organization’s dependency on him, the decentralized structure of Constellation and its unique culture are now part of the organization’s DNA and the employees have been educated that way and allocate capital in the same fashion Leonard does.

The known investment advisory company Ruane Cunniff, founded by Warren Buffett associate Bill Ruane and By Rick Cunniff, is known for its long term investment approach. Ruane Cunniff’s Sequoia Fund has been invested in Constellation for approximately eight years and has a great relationship with its management. In fact, in the last annual general meeting of Constellation, Larry Cunningham mentioned Will Pan, a Ruane Cunniff Analyst, as one of the two analysts he was assisted by in posting the questions during the meeting.

David Poppe, the former president and CEO of Ruane Cunniff, now President at Giverny Capital Asset Management and a participant in the last white paper, says he doesn’t think it’s crazy to compare Mark Leonard to Warren Buffet. Leonard is a very intelligent man, but he is also somewhat of an inspirational figure. People like working with him and working for him. He has built a very talented and long-lasting committed team in the next level below him.

‘’.. employees define a good workplace in large part on the basis of whether “my boss is fair”. Every

decision and action regarding people in which a manager engages is watched by a jury of manager’s

peers and those reporting to her”1

-

- Promotion from within

Last but not least, another significant element of trust is promoting from within the company. In CSI promoting from within is a consistent habit with about 75% of senior managers promoted from within as of 2020

2Execution

-

- Results orientation

Every single person I spoke with told me that if an employee cannot deal with his or her managers measuring their performance constantly on actual results, he or she will not survive. Managers don’t care about the amount of hours you work or the location from which you work (even pre COVID-19); they care about your execution. In order to execute, an employee at Constellation must be very curious and work hard.

-

- Clear metrics

Leonard is well known for measuring the company’s performance by Return on Invested Capital (ROIC) + Organic growth. ROIC is a central metric at the organization, and employees are measured on their contribution to ROIC performance. Business Units (BU) performance, in the figure of ROIC and IRR prediction versus Reality, are key metrics and are measured over the long term. A portfolio manager who excels in ROIC contribution to the firm can earn large sums of money. In order to keep the pace of high ROIC, the PM’s are incentivized to use the cash that portfolio companies generate and invest it in additional companies with the ability to generate high ROIC. This is how Constellation’s well run mechanism is preserved.

-

- A start-up mentality

An important part of this execution mentality is hidden in another characteristic of the company, an ambition of many other mostly tech companies to keep the small start-up company feeling (remember the Amazon “day 1” mentality embraced by Jeff Bezos). CSI founded in light of Mark Leonard’s vision and experience from VC that software companies have to be agile and flexible in their very dynamic industry. The structural way to do that was to form the unique decentralized structure of Constellation

1The Culture Cycle by James Heskett – Page 88

where for each group there is its own key executives so decisions are made quite fast compared to other players, kind of a feeling of an eternal start-up – an important part of a tech company culture. In the fabulous book “The Culture Cycle”, failure to maintain a small-company feel is mentioned as a diluter of culture. “Cultures are fostered in small groups. They are reinforced and easier to sustain with the kind of peer pressure and transparency that are a part of such working environments.”2

-

- Keep it simple

Even with hundreds of independent entities, the organization obtains a unified spirit. As I continued to delve into the matter, I found that even though operating groups are separate and independent, there is a unity among employees and former employees and they speak in quite a similar fashion, sometimes like you can hear Mark Leonard himself. This unity is very important for this acquisition machine where employees from across the globe understand the company’s philosophy well and what it looks for. A fascinating thing is that a mission that apparently looks complicated, constantly acquiring software companies in different industries, acquisition targets that match specific quantitative and qualitative categories, and the company structure that is very unusual in the business landscape, looks very clear to a CSI employee who in many cases is a young individual who has just graduated from university. The fact that this structure is so rare in companies of CSI’s size while being so profitable shows that those methods that are rooted throughout the organization and might be very obvious to an employee are very hard to implement.

3Long term horizon

-

- Employees as a long term partners:

CSI is known in its equity culture, distributing stocks to employees. As known and researched before, employee who owns stocks for long term acts more like an owner. Management itself holds a significant amount of equity with Mark Leonard the 5th major investor in the company.

“In addition to our long term sophisticated investors, we also have a second constituency of less financially oriented long-term investors, including some of our employee shareholders. Our employee bonus plan requires that all employees who make more than a threshold level of compensation invest in CSI shares and hold those shares for an average of at least 4 years. In practice, their average hold period has been much longer.” Mark Leonard, Constellation Software President’s letter 2013

It’s very important for the management that employees will feel like owners. As an example, when Topicus.com has been spun off from Constellation in February 2021, the policy of employees invested their bonuses in the stock has been changed accordingly and Tupicus employees invest them now in the new share.

2The Culture Cycle by James Heskett – Page 84

David Poppe says senior employees seem to feel like true partners. They have the ability to have a lot of influence, to be able to allocate capital to businesses they find are good, to build the companies they want to build, and to have a lot of responsibility. They run their own businesses and they have a lot of autonomy. Those things are quite unusual and he thinks that attracts people. There is a great partnership mentality at Constellation according to his words. In addition, the fact that Mark is an inspirational leader who stands out makes people really want to be associated with him.

Poppe says that the way the employees interact with each other is quite special. He notes that this is a really collegial cooperative environment. You can feel that even in the annual general meeting in the way the management tries to learn from one another. They are interested in learning from the experience of other parts of the organization and are willing to implement those lessons

-

- Portfolio companies as partners:

The mentality of investment in portfolio businesses for life is another notable part of Constellation Software – No matter if it’s a private company or a minority shares in a public one.

David Poppe says that Constellation really made a home for these small software companies. People want to be a part of that company. Similar to Berkshire Hathaway, senior management stays forever. People want to stay even after they earn enough money to support their families for 50 years.

A caveat to that similarity to Berkshire is that Constellation is much more active than Berkshire. The first tries to improve and fix businesses while the second is much more hands off

-

- Shareholders as partners:

Constellation Software, who sees itself as a long term owner of its portfolio companies, considers its shareholders as long term owners. This attitude is well expressed in the management’s communication with the company shareholders. One of Mr. Leonard’s duties is his open dialog with shareholders, his detailed letters to shareholders and answers for investor’s questions published on the company website. Leonard creates the feeling among the shareholders that each one is equal, even shareholders with a low holding, and takes into consideration the various profiles of different shareholders: An example in mind is Leonard’s decision to maintain a dividend policy announced under the pressure of a private equity who owned substantial shares in the past and taking into consideration the interest of investors who bought out these shares from the PE.

“The dividend was a tactic, not a strategic move. It broadened the appeal of our stock and thereby helped us find an exit for our private equity investors. We appreciate the confidence in CSI that many of the new investors expressed in buying the PE shares. We recognise that these investors bought, in part, because of the dividend and the implicit promise of continued yield. Eliminating it would disenfranchise a group of shareholders to whom we owe our independence. That wouldn't sit right with me and many of the senior management team, so I don’t see it happening” Mark Leonard, Constellation Software President’s letter 2012

David Poppe says you can feel that management really cares about investors. In the investor meetings he has gone to, there were long breakouts where you have a chance to engage with the management team and not only the CEO, CFO, and the IR team. You can really meet the operating people. And that’s not something they do only for the large shareholders as they do this in a regular public meeting

Mark Leonard really sees shareholders as partners and as such, he also expects them to conduct proper research and understand the company and its performance.

“The most impressive investors are those with a nuanced understanding about business. They get that through obviously consuming all the stuff that’s publicly available but they often get it through non public sources as well. They build relationships with employees, they talk to costumers, they go to trade shows, they follow all of the unconventional so call “scuttlebutt” type sources..” Mark Leonard, Constellation Software AGM 2021.

Proof for the company’s long term shareholders is that the second major investor in the company is the well known investor Chuck Akre. Mr Akre is known for his very long term investment horizon. He holds on to companies for decades. Notable examples are his holdings in Berkshire Hathaway and Markel Corporation which he has owned since 1977 and 1991, respectively. In his very concentrated portfolio, holdings are very meaningful and will seal its portfolio’s fate over time.

4Conservatism

-

- Conservative predictions

Constellation’s capital allocators have a shared conservative nature in making predictions. Not paying for acquired companies’ growth is one such rule of thumb in Constellation that helps avoid over optimism.

-

- Staying within you circle of competence

One might think that a big difference between Berkshire and Constellation is the fact that the latter invests in the dynamic tech industry. Buffett said many times in the past that technology in general is out of his circle of competence, and even though Berkshire invests now more meaningfully in tech companies (some of these probably made by Buffett’s successors), Berkshire’s portfolio was generally low weighted in that field for many years. The paradox is that in this big difference lies an even bigger similarity. In Constellation, similar to Berkshire, the portfolio managers invest inside their circle of competence. Software is a field of expertise for Leonard even prior to Constellation’s inception and the portfolio managers recruited specialize in this field and concentrate on it day by day.

-

- SLow valuations

As appeared to me, Constellation is a classic old fashioned value investor. Constellation invests mostly in small businesses (several million dollars) but mature ones that don’t need to invest much in R&D and growth expenditures, in niche markets and not very popular ones – that way it can be one of the only bidders for the businesses acquired and pay relatively low purchase prices. Since Constellation invests in mature companies operating in mature industries, growth is moderate or even non-existent, and as mentioned before Constellation will not pay for growth predictions. Constellation would bid for lower prices compared to other investors but its reputation for preserving the acquired company’s brand and key people and investing for life in contrast to some private equities, puts it in a more attractive position that allows it to suggest such low prices. Very similar to Berkshire, Constellation would offer one price to the potentially acquired company which it can accept or not. The price that could look as too low for the acquired company’s owner in the first place, many times appeared as reasonable after making many negotiations with other private equity firms and he or she might come back to accept Constellation’s offer after a while. Another point that should be made is that the price Constellation is able to get is a function of the fact it doesn’t invest in some of the “hot high-tech industries” such as cyber security and AI but more on traditional software companies which own the software underlying the system of a country club operation. Constellation acquires software companies in vertical markets that provide an especially essential service in the specific market. Usually that service constitutes a very low percent of the total expenses in the respective industry and its value is much higher than its cost. This aspect might remind the reader of other well known investors that expressed the same way about investing such as Marathon Asset Management in the UK and John Hempton in Australia.

-

- Contrarianism

When reading Leonard’s letter and listening to him, I noticed repetitive contrarianism signs, and it doesn’t change as years pass:

“One of the causes for declining organic revenues is outside of our control: U.S. housing starts declined approximately 28% in Q1 2007 compared to the same period in 2006, and that seems to have depressed spending amongst our homebuilding, construction and building products related customers. For the most part, we are pleased with how our homebuilding and related businesses have responded to the tougher operating environment. We continue to seek acquisition prospects among software companies that service these currently depressed markets.” Constellation Software letter to shareholders, 2007

“One of the first things I did on the hills of the early lockdown was reach out some of our best competitors and offer them minority investments… ” Mark Leonard, Constellation Software AGM 2021

“It’s not like people bring us opportunities, we go looking for opportunities. And when do we go look? We go look when other people aren’t looking… You got to be contrarian to get superior results” Mark Leonard, Constellation Software AGM 2021

Final words:

Constellation Software has a terrific history and its culture was praised by many. In addition, one cannot ignore the company’s great financial results for decades and its stock’s over performance. However, I would like to say that during the research process I haven’t found a company with a perfect culture, and I doubt if there is one. Even in CSI I found satisfied and less satisfied employees, managers who mentioned operating groups with relatively high employee turnover compared to others, dissatisfied customers and less successful acquisitions – but, the clear picture is this is a company with a positive successful corporate culture that enhances the competitive advantage of the company for many years

Two other values that I considered adding but were left outside were – 1. Curiosity, which I touched briefly in the paper and 2. Modesty, which is especially noticeable in top management’s approach and reasonable compensation packages.

Further reading:

I would recommend anyone who wants to learn about the company and its culture to read the sources I used in this white paper. These include Mark Leonard’s letters to shareholders, investors meeting records and transcripts, Larry Cunningham’s books “Dear Shareholder: The best executive letters from Warren Buffett, Prem Watsa and other great CEOs,” and “Margin of Trust,” and “The 10th Man,” articles about Constellation Software and its subsidiaries.

Two main sources used as theoretical guidelines for culture in general were “HBR’s 10 Must Reads: On Building a Great Culture,” and the book “The Culture Cycle,” by James Heskett.